Blog Details

How Is Personal Loan EMI Calculated?

Personal Loan EMI is calculated using a standard mathematical formula that considers the loan amount, interest rate, and repayment tenure. The formula distributes the total payable amount (principal + interest) into equal monthly installments over the selected loan period.

Calculating the EMI for a personal loan can be complex because it depends on several factors such as loan amount, interest rate, and tenure. For individuals who are not familiar with the detailed EMI calculation process, manual computation can be confusing and time-consuming. In such cases, a personal loan interest rate calculator is highly useful.

- It performs advanced monthly installment estimations instantly, helping save valuable time.

- It reduces the risk of calculation errors and ensures accurate results.

- It helps borrowers plan their repayment strategy in advance by providing precise and reliable figures.

What Is Personal Loan EMI?

A Personal Loan EMI (Equated Monthly Installment) is the fixed monthly payment a borrower makes to repay a personal loan over the selected repayment period. Each EMI consists of two parts: a portion of the principal amount and the applicable interest. The EMI amount is determined using a standard calculation formula based on the total loan amount, interest rate, and loan tenure. Because the installment remains consistent throughout the repayment term, borrowers can plan their monthly budget with confidence, knowing the exact amount payable until the loan is completely repaid.

Must Read: Personal Loan vs Credit Card Which One You Choose

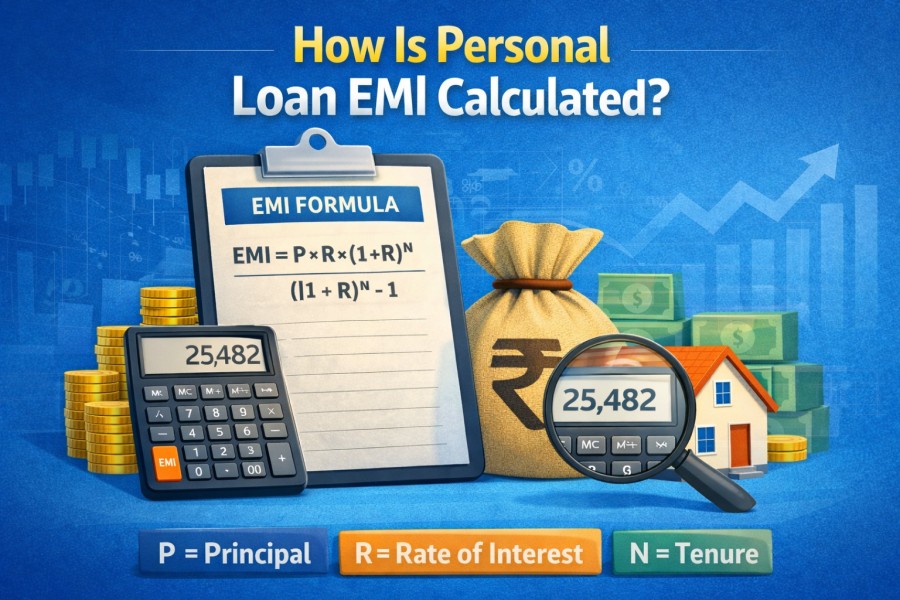

What Is the Formula to Calculate EMI?

Calculating the EMI for a personal loan involves applying a standard formula that is commonly used across all online EMI calculators. Loan Quantum personal loan EMI calculator follows this widely accepted calculation method to provide an accurate estimate of the monthly installment payable on your loan.

Meaning of P, R, and N in EMI Formula

The interest rate (R) must be converted into a monthly rate by dividing the annual rate by 12 before applying the formula.

EMI = [P × R × (1+R)^N] / [(1+R)^N − 1]

EMI, Equated Monthly Payment

P - Principal amount

R - Rate of interest

N - Tenure

This personal loan EMI calculator formula can be used to obtain the EMI for any loan amount.

Example of Personal Loan EMI Calculation

For a ₹5 lakh personal loan at 11% interest for 60 months, the EMI is calculated using the standard EMI formula, resulting in a monthly installment of ₹10,871 and a total interest payable of ₹1,52,273 over the loan tenure.

| Loan Amount (P) | Annual Interest Rate | Tenure (N) | Monthly EMI | Total Interest Payable |

|---|---|---|---|---|

| ₹1 Lakh | 10.75% | 12 months | ₹ 8,827 | ₹ 5,924 |

| ₹1 Lakh | 10% | 60 months | ₹ 2,124 | ₹ 27,440 |

| ₹5 Lakhs | 11% | 60 months | ₹ 10,871 | ₹ 1,52,273 |

| ₹10 Lakhs | 12% | 60 months | ₹ 22,244 | ₹ 3,34,640 |

| ₹15 Lakhs | 13% | 60 months | ₹ 34,130 | ₹ 5,47,800 |

₹5 Lakh Loan Example

A ₹5 lakh personal loan is suitable for individuals who have clear financial requirements and the repayment capacity to manage monthly installments comfortably. Since it is a considerable loan amount, it should be taken after careful financial planning. Below are the categories of borrowers for whom it is most appropriate:

- Salaried individuals with consistent income: Those earning ₹50,000 or more per month with stable employment can use a ₹5 lakh loan to manage significant expenses without disturbing their long-term savings. It works well for borrowers who can easily accommodate EMIs within their monthly budget.

- Families preparing major expenses: Costs related to weddings, medical emergencies, overseas travel, or higher education may exceed available savings. A ₹5 lakh personal loan can help meet these large financial commitments while offering flexible repayment options.

- Self-employed individuals for personal expenses: Although business loans are more suitable for professional requirements, self-employed applicants may choose a ₹5 lakh personal loan to fund personal needs such as home renovation, debt consolidation, or high-value purchases.

Must Read: What is the EMI For 12 Lakh Personal Loan For 5 Year

Factors That Affect Personal Loan EMI

Several factors influence a personal loan EMI, including the loan amount, interest rate, and repayment tenure. In addition, lenders assess multiple financial parameters before determining loan eligibility and applicable interest rates.

- Income: Banks evaluate a borrower’s repayment capacity based on monthly income. The approved loan amount depends on income level, age, and selected tenure.

- Employment Details: The lender considers whether the applicant is employed in the public sector, private sector, or is self-employed. Job stability, employment type, and total years of work experience play an important role in loan approval and EMI terms.

- Credit Score: Financial institutions review your creditworthiness through your credit score. A score above 800 generally qualifies borrowers for lower and more competitive interest rates.

- Debt-to-Income (DTI) Ratio: Ideally, your total EMIs should not exceed 40–50% of your net monthly income. For example, if you earn ₹80,000 per month and pay ₹45,000 toward EMIs, your DTI ratio is close to 60%. In such cases, lenders may apply a higher interest rate. A lower DTI ratio, however, improves your chances of securing better loan terms.

Must Read: Pre - Approved Personal Loan Guide

EMI Calculation Table for Different Loan Amounts

The EMI (Equated Monthly Installment) on a loan is determined by three primary factors: the principal amount, the applicable interest rate, and the repayment tenure. For loan amounts ranging from ₹10 lakh to ₹50 lakh with interest rates between 9% and 15% over a tenure of 5 to 20 years, the monthly EMI can vary from approximately ₹9,000 to more than ₹45,000.

EMI Calculation Table

| Loan Amount(₹) | Interest Rate(p.a.) | Tenure(Years) | Estimated EMI(₹) |

|---|---|---|---|

| 1,00,000 | 12% | 1 | 8,885 |

| 5,00,000 | 12% | 3 | 16,607 |

| 10,00,000 | 10% | 5 | 21,247 |

| 10,00,000 | 15% | 5 | 23,790 |

| 25,00,000 | 9% (Home) | 15 | 25,343 |

| 25,00,000 | 9% (Home) | 20 | 22,493 |

| 50,00,000 | 9% (Home) | 20 | 44,986 |

| 25,00,000 | 12% | 10 | 71,735 |

Must Read: What is Instant Personal Loan and How Does it Work

Why Calculating EMI in Advance Is Important

Calculating your personal loan EMI in advance provides a clear financial roadmap for managing repayments throughout the loan tenure. It prevents unexpected financial strain and helps you plan your monthly budget more effectively.

By understanding your EMI amount beforehand, you can choose the right loan amount and repayment tenure based on your income and financial capacity. This lowers the risk of payment defaults and helps maintain a healthy credit score. With LoanQuantum’s easy-to-use Personal Loan EMI Calculator, you can accurately compute your monthly EMI based on the selected loan amount and preferred tenure, ensuring better financial planning.

Must Read: Calculate Loan Amount Online

Conclusion

Understanding how Personal Loan EMI is calculated helps borrowers make informed and responsible financial decisions. Since EMI computation depends on the loan amount, interest rate, and repayment tenure, evaluating these factors carefully ensures better budget planning and repayment management. By calculating your EMI in advance, you can choose a suitable loan structure that aligns with your income and financial capacity while avoiding unnecessary repayment stress.

To simplify the process, you can use the LoanQuantum Personal Loan EMI Calculator to instantly estimate your monthly installment and plan your loan repayment with clarity and confidence.

Calculate your Personal Loan EMI instantly with the LoanQuantum EMI Calculator and plan your repayments with confidence.

Frequently Asked Questions

The interest rate on Personal Loans may vary based on revisions made by the Bank or regulatory changes introduced by the RBI from time to time.

Personal loan repayment is made through Equated Monthly Installments (EMIs), which are paid every month until the loan is fully settled.

The EMI of a personal loan depends on the following key factors:

- Principal Amount: This is the total loan amount borrowed from the bank. A lower principal results in a lower EMI, while a higher principal increases the EMI.

- Interest Rate: This is the rate at which the bank offers the personal loan. A higher interest rate leads to a higher EMI, and a lower rate reduces the EMI amount.

- Loan Tenure: Tenure refers to the repayment period of the loan. A longer tenure lowers the monthly EMI but increases total interest paid, whereas a shorter tenure increases EMI but reduces overall interest cost.

When you purchase a product using the EMI option on a credit card, your available credit limit is immediately reduced by the total purchase value. Similar to a home loan or personal loan EMI, you repay the amount in monthly installments that include both principal and interest. Over time, the outstanding balance reduces gradually until the full amount is repaid. Credit card EMI is calculated using the reducing balance method.

If you skip your EMI, the lender may charge a late payment penalty and additional interest. Your personal loan EMI will remain unpaid and will be added to your outstanding loan balance.