Blog Details

Business Loan vs Business Credit Line: Key Differences Explained

Access to funding plays a major role in helping enterprises manage operations, expand services, purchase equipment, and maintain healthy cash flow. Whether you are running a growing venture or launching a new startup, choosing between a business loan and a business credit line can significantly impact your financial planning.

Many entrepreneurs compare these financing solutions before making a borrowing decision. Understanding how each option works can help determine which one aligns better with your business goals.

What Is the Difference Between a Business Loan and a Business Credit Line?

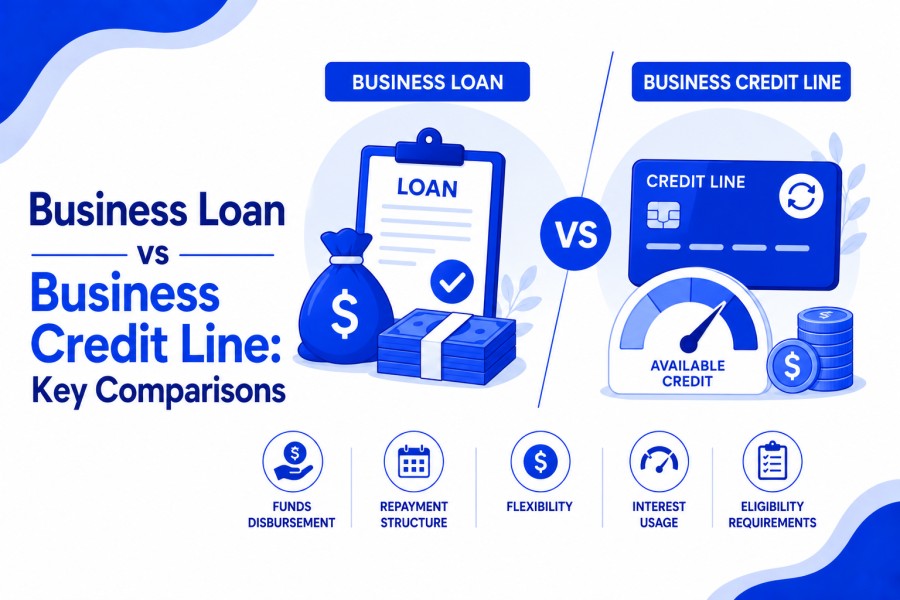

A business loan provides a lump-sum amount that is disbursed upfront and repaid through fixed installments over a specific tenure. It is commonly used for long-term investments, expansion projects, machinery purchases, or infrastructure development.

A business credit line, on the other hand, offers flexible access to funds up to a pre-approved limit. Borrowers can withdraw money as needed and pay interest only on the utilized amount. While both financing methods support growth, their structure and repayment models differ considerably.

When Should Small Businesses Choose a Business Loan?

A business loan is often suitable when a company requires a large amount of capital for planned expenses. Common situations include:

- Business expansion

- Equipment purchases

- Office renovation

- Inventory stocking

- Franchise development

- Working capital requirements

Using a business loan calculator helps estimate repayment schedules and understand overall borrowing costs before applying. Businesses that prefer predictable monthly obligations often choose term financing because the business loan EMI remains fixed throughout the repayment period.

Why Do Startups Consider a Business Credit Line?

Startups frequently face fluctuating operational expenses and uncertain revenue cycles. A business credit line provides flexibility by allowing owners to access capital as needed. Benefits for startups include:

- Better cash flow management

- Quick access to emergency funds

- Interest charged only on utilized credit

- Flexible withdrawals and repayments

- Improved liquidity during growth phases

This financing model is particularly useful for seasonal businesses or enterprises experiencing irregular revenue patterns.

How Does Repayment Work for Both Financing Options?

Repayment structures vary significantly between the two choices.

Business Loan Repayment

With a business loan:

- Borrowers receive the entire sanctioned amount upfront.

- Monthly installments are fixed.

- Interest is calculated on the total borrowed amount.

- Loan tenure is predetermined.

Many borrowers use a business loan calculator to evaluate monthly obligations and select a comfortable repayment period.

Business Credit Line Repayment

With a credit facility:

- Funds are withdrawn only when required.

- Interest applies to the amount utilized.

- Credit becomes available again after repayment.

- Borrowers enjoy revolving access to capital.

This flexibility can be beneficial for managing short-term working capital needs.

Which Option Offers Better Cash Flow Management?

Cash flow is one of the most important factors of corporate sustainability. A business credit line generally provides greater flexibility because companies borrow only what they need. This helps reduce unnecessary interest expenses and supports day-to-day operations.

However, if a business has a clearly defined project requiring significant investment, a business loan may be more efficient because it offers immediate access to a larger amount of capital. When comparing financing solutions, entrepreneurs should carefully compare the loan structure with their revenue patterns and operational requirements.

Is a Business Loan More Cost-Effective Than a Credit Line?

The answer depends on borrowing behavior and funding requirements. A business loan may prove more economical for:

- Large one-time investments

- Expansion projects

- Asset acquisition

- Long-term business planning

A credit line may be advantageous for:

- Seasonal expenses

- Inventory purchases

- Payroll management

- Unexpected operational costs

Evaluating interest rates, payback terms, and processing fees will help you choose the most cost-effective financing option.

How Can Digital Lending Simplify Business Financing?

The rise of digital lending has transformed how enterprises access capital. Modern lending platforms provide:

- Faster approvals

- Simplified documentation

- Online applications

- Quick disbursement

- Transparent eligibility assessment

Many lenders now offer instant eligibility checks and financing comparisons, making it easier for entrepreneurs to identify suitable funding options. Digital lending solutions have become especially valuable for startups and small businesses seeking quick access to working capital.

Which Financing Option Is Best for Small Businesses?

For many small business owners, the right choice depends on operational needs. A business loan is generally suitable when:

- A fixed amount is needed

- Expansion plans are clearly defined

- Predictable repayment schedules are preferred

A business credit line may be more suitable when:

- Cash flow fluctuates regularly

- Ongoing access to capital is required

- Funding needs are unpredictable

The best financing strategy aligns with business objectives, revenue cycles, and future growth plans.

Can a Business Loan Calculator Help Before Applying?

Absolutely. A business loan calculator helps entrepreneurs:

- Estimate monthly installments

- Understand total repayment costs

- Compare borrowing scenarios

- Plan budgets more effectively

- Evaluate affordability before applying

Using financial planning tools can reduce borrowing risks and improve decision-making.

Conclusion

Choosing between a business loan and a business credit line requires careful evaluation of funding requirements, repayment capacity, and business objectives. While a term loan offers structured financing with predictable business loan EMI, a credit line provides flexibility and ongoing access to funds. For startups, growing enterprises, and small business owners, understanding these differences can lead to better financial decisions and stronger long-term growth. With the increasing availability of digital lending solutions, comparing financing options has become easier than ever, helping businesses secure the right funding at the right time.

Ready to choose the right financing solution for your business? Compare business loan and credit line options with LoanQuantum and find funding that supports your growth, cash flow, and long-term goals.

Frequently Asked Questions

A business credit line is generally better for cash flow management because businesses can access funds whenever needed and pay interest only on the borrowed amount.

The cost depends on usage. A credit line may be more cost-effective for short-term borrowing, while a business loan may offer better value for large, long-term financing needs.

Unlike a business loan, a credit line usually offers more flexible repayment terms, depending on the amount utilized and the lender's policies.

Yes, many businesses use both financing options simultaneously. A business loan can fund expansion projects, while a credit line can help manage day-to-day operational expenses.

Yes, businesses with seasonal revenue patterns often benefit from flexible borrowing because they can access funds during slower periods and repay them during peak seasons.