Blog Details

What is the EMI for 12 Lakh Personal Loan for 5 Years?

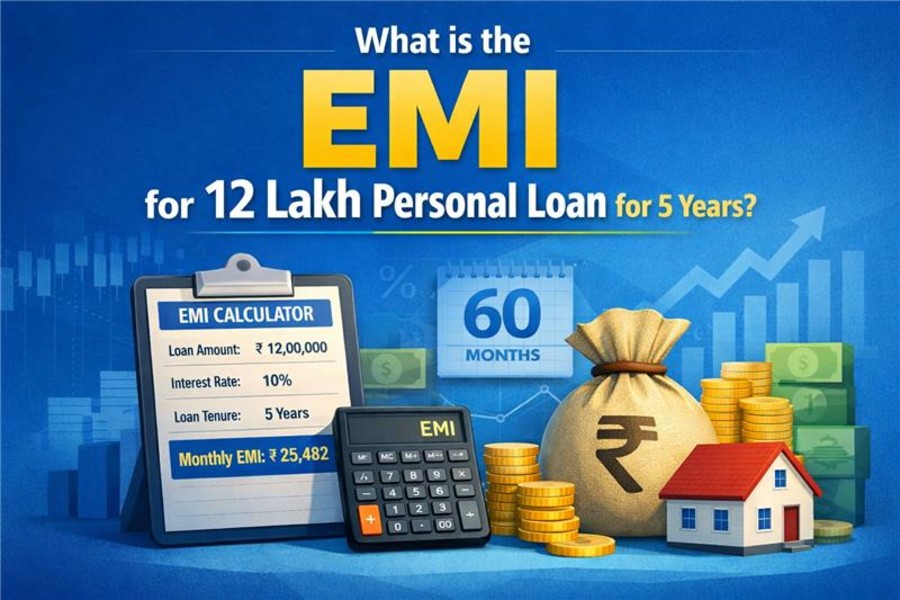

EMI for ₹12 Lakh Personal Loan for 5 Years at Different Interest Rates

If you're planning to take a ₹12 lakh personal loan for 5 years, your EMI will typically range between ₹24,900 and ₹28,500 depending on the interest rate offered by the lender. Even a small rate difference can impact your total repayment by lakhs over time.

EMI Formula:

EMI = P × r × (1+r)^n / ((1+r)^n − 1)

Where:

- P = Loan amount

- r = Monthly interest rate

- n = Number of months

Here’s an EMI comparison table for a ₹12 lakh personal loan for 5 years, showing monthly installments, total repayment amount, and total interest payable at different interest rates.

| Interest Rate | EMI (Approx) | Total Repayment | Total Interest |

|---|---|---|---|

| 9% | ₹ 24,900 | ₹14.9 Lakh | ₹2.9 Lakh |

| 10% | ₹ 25,500 | ₹15.3 Lakh | ₹3.3 Lakh |

| 12% | ₹ 26,700 | ₹16 Lakh | ₹4 Lakh |

| 15% | ₹ 28,500 | ₹17.1 Lakh | ₹5.1 Lakh |

Here’s a detailed breakdown of EMI calculation, total interest payable, eligibility criteria, and ways to reduce your loan burden.

Recent blog: Best Tips for Getting Approved for a Personal Loan

How Interest Rates Affect Your ₹12 Lakh Personal Loan

Interest rate is the biggest factor that determines your monthly EMI and total repayment amount. Even a small difference of 1–2% can significantly impact your total cost of loan over 5 years.

For example:

- At 9% interest, EMI will be approximately ₹24,900 per month.

- At 10% interest, EMI increases to around ₹25,500.

- At 12% interest, EMI goes up to roughly ₹26,700.

- At 15% interest, EMI can reach around ₹28,500.

That’s a difference of nearly ₹3,500 per month between 9% and 15%.

Higher interest rates mean:

- Higher EMI

- Higher total repayment

- Increased financial burden

Lower interest rates mean:

- Lower EMI

- Better affordability

- Reduced overall loan cost

Your interest rate is influenced by:

- Credit score

- Monthly income

- Employment stability

- Existing debts

- Lender policies

Borrowers with a credit score above 750 usually get better rates, while lower scores may result in higher interest charges.

Recent blog: Get an Instant Personal Loan with a Low CIBIL Score

Total Interest Payable on a ₹12 Lakh Loan Over 5 Years

Many borrowers focus only on EMI but ignore the total cost of borrowing. Over 5 years, you will repay much more than ₹12 lakh due to accumulated interest.

Here’s an approximate idea:

- At 9% interest → Total repayment around ₹14.9 lakh

- At 10% interest → Total repayment around ₹15.3 lakh

- At 12% interest → Total repayment around ₹16 lakh

- At 15% interest → Total repayment around ₹17.1 lakh

This means you may pay ₹2.9 lakh to ₹5.1 lakh purely in interest over 5 years.

Apart from interest, lenders may also charge:

- Processing fees (1–3%)

- Prepayment or foreclosure charges

- Late payment penalties

- GST on applicable charges

Always calculate the total repayment amount before finalizing your loan to understand the real cost.

Recent blog: How Does Age Affect Personal Loan Eligibility?

Tips to Reduce Your Loan Burden

A ₹12 lakh loan is manageable if planned properly. Here are smart ways to reduce financial stress:

- Maintain a Strong Credit Score: A higher credit score can help you secure a lower interest rate, directly reducing EMI and total interest paid.

- Compare Multiple Lenders: Don’t accept the first offer. Compare interest rates, processing fees, and hidden charges before deciding.

- Choose the Right Tenure: A longer tenure reduces EMI but increases total interest. A shorter tenure increases EMI but reduces total cost. Choose what suits your income stability.

- Avoid Over-Borrowing: Borrow only what you need. Higher principal means higher EMI and more interest.

- Consider Prepayment: If your lender allows partial loan prepayment without heavy charges, paying extra during bonus months can reduce interest burden significantly.

Smart planning can save you lakhs over the loan duration. You can also use a ₹12 lakh personal loan EMI calculator to get exact monthly installment figures based on your credit profile.

Eligibility Criteria for ₹12 Lakh Personal Loan

Before applying, make sure you meet basic lender requirements. Though criteria vary by institution, general eligibility includes:

Age Requirement: Typically, between 21 and 60 years.

Income Requirement: Most lenders prefer a minimum monthly income of ₹25,000 to ₹30,000 for a ₹12 lakh loan. Higher income improves approval opportunities.

Credit Score: A score above 700 is usually preferred. For best interest rates, aim for 750+.

Employment Type:

- Salaried individuals with at least 6–12 months of job stability

- Self-employed individuals with consistent business income

Documents Required:

- Aadhaar & PAN card

- Salary slips (last 3 months)

- Bank statements (last 6 months)

- Income proof for self-employed applicants

Meeting eligibility criteria not only increases approval chances but also helps secure better interest rates.

Related blog: Personal Loan vs. Credit Card: Which One Should You Choose?

How to Reduce EMI on a ₹12 Lakh Personal Loan?

If EMI feels high, there are ways to bring it down:

Opt for Longer Tenure: Increasing tenure spreads repayment over more months, reducing EMI amount. However, remember this increases total interest.

Improve Your Credit Score Before Applying: If your score is low, take 3–6 months to improve it before applying. Paying credit card dues on time and reducing outstanding balances helps.

Apply with a Co-Applicant: Adding a co-applicant with stable income can improve loan eligibility and sometimes reduce interest rate.

Negotiate with Lender: If you have strong financials, you may negotiate interest rates or processing fees.

Refinance Later: If interest rates drop in the future, consider refinancing your loan to reduce EMI.

Even a small EMI reduction of ₹1,000 per month saves ₹60,000 over 5 years.

Blog might you have missed: Salary-Based Personal Loans: Benefits, EMI Tips & Approval

Why Choose LoanQuantum for a 12 Lakh Personal Loan for 5 Years

Choosing the right platform is as important as choosing the right lender. LoanQuantum simplifies the borrowing process by helping you compare multiple loan options in one place.

With LoanQuantum, you get:

- Competitive interest rate comparisons

- Access to multiple lender offers

- Fast online process with minimal paperwork

- Transparent charges

- Time-saving application experience

Related blog: Top Benefits of Applying for a Personal Loan Online

Whether you are planning a medical emergency, home renovation, debt consolidation, or personal expenses, understanding your EMI and total repayment is the first step toward smart borrowing.

A ₹12 lakh personal loan over 5 years can be manageable if you secure a good interest rate, plan your EMI wisely, and choose the right financial partner.

Make informed decisions, compare loan rates and options carefully, and ensure the loan fits comfortably within your monthly budget before applying.

Interest rates and EMIs are indicative and may vary based on lender policies and borrower profile.

Use LoanQuantum’s smart comparison tool to calculate your exact ₹12 lakh loan EMI, compare real-time lender offers, and secure the lowest interest rate today.

Frequently Asked Questions

The EMI for a ₹12 lakh personal loan for 5 years typically ranges between ₹24,900 and ₹28,500 per month, depending on the interest rate. At 12% interest, the EMI is approximately ₹26,700 per month.

The total interest payable on a ₹12 lakh loan for 5 years can range from ₹2.9 lakh to ₹5 lakh, depending on the interest rate. Higher interest rates significantly increase the total repayment amount.

Most lenders prefer a minimum monthly salary of ₹25,000 to ₹30,000 for a ₹12 lakh personal loan. Higher income and a strong credit score improve approval chances and help secure better interest rates.

Yes, it is possible, but you may be charged a higher interest rate. A credit score above 700 is generally preferred for better approval chances and lower EMI.

You can reduce EMI by choosing a longer tenure, improving your credit score before applying, comparing lenders, or negotiating a lower interest rate. Even a small rate reduction can significantly lower your monthly payment.