Blog Details

What Happens When You Miss a Personal Loan EMI?

Life doesn’t always go as planned. A sudden expense, a delayed salary, or an emergency, and before you know it, you’ve missed your personal loan EMI.

Whether you are a first-time borrower, a salaried employee, or someone using a personal loan calculator for planning, understanding the impact of missed EMIs is crucial for maintaining financial health.

Let’s break it down in a simple, practical way so you know exactly what happens and how to stay in control.

What is Personal Loan EMI in simple terms?

A personal loan's EMI is the exact amount you repay each month. It includes:

- A portion of your loan principal

- The interest charged by the lender

Your EMI is calculated based on:

- Loan amount

- Interest rate

- Tenure

This is where a personal loan calculator becomes extremely useful. It helps you estimate your EMI in advance and choose a repayment plan that actually fits your monthly budget, especially important for salaried employees managing fixed income.

Why Proper EMI Planning Matters?

Taking a personal loan is easy today, but managing it responsibly is what truly matters. Many borrowers focus only on getting quick approval and overlook whether the EMI actually fits their monthly budget. This is where proper EMI planning becomes essential.

When you calculate your personal loan EMI in advance using a personal loan calculator, you get a clear picture of how much you’ll need to pay every month. This helps you avoid over-borrowing and ensures your loan remains affordable throughout the tenure.

For salaried employees, this is especially important because income is fixed and expenses are often predictable. If your EMI takes up too much of your salary, even a small financial disruption, like a medical emergency or delayed salary, can lead to missed payments.

Proper planning also improves your chances of meeting loan eligibility criteria in the future. Lenders prefer borrowers who show financial discipline and manage their EMIs smoothly. On the other hand, poor planning can lead to:

- Higher financial stress

- Increased dependence on credit

- Difficulty in managing other expenses or savings

Another important factor is choosing the right option among different loan types. For example, a flexi personal loan may offer flexibility in repayment, but it still requires careful planning to avoid unnecessary interest costs.

In simple terms, EMI planning is not just about calculation; it’s about ensuring your loan fits comfortably into your life without affecting your financial stability or long-term goals like investments and tax savings.

Related blog: Top Reasons Why Your Personal Loan Gets Rejected

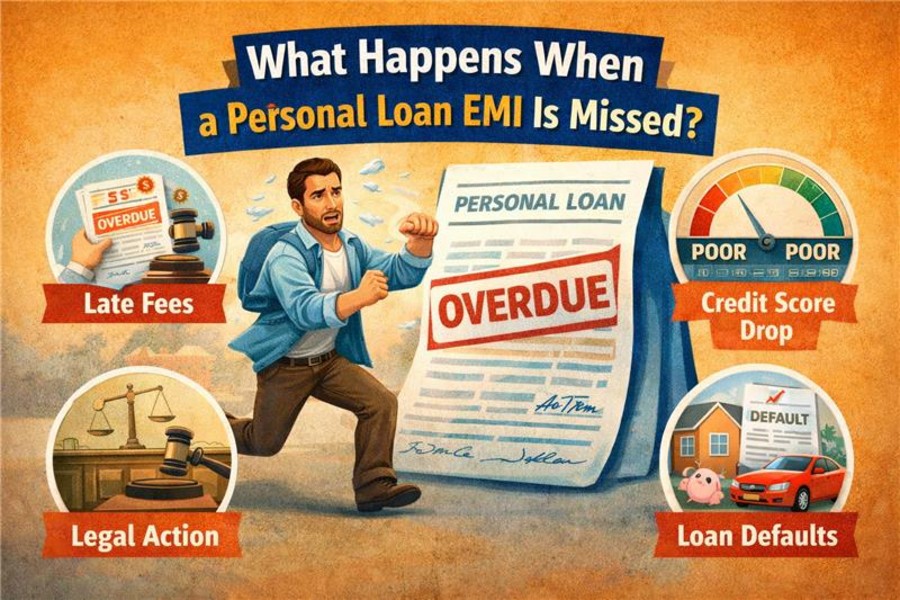

What Really Happens When You Miss an EMI?

Missing an EMI isn’t just about one payment; it triggers a chain reaction. Here’s what typically happens:

1. Immediate Penalty Charges

The moment your EMI is missed:

- The bank adds a late payment fee

- Penal interest starts accumulating on the overdue amount

Even if the amount seems small, these charges build up quickly if not cleared. Think of it like a snowball, small at first, but it grows faster than expected.

2. EMI Bounce Charges (If Auto-Debit Fails)

If your EMI is set on auto-debit and your account has insufficient funds:

- The transaction fails

- You are charged a bounce fee

This is very common among salaried employees, especially when expenses and salary dates don’t align properly.

3. Your Credit Score Takes a Hit

This is where the real impact begins.

Your repayment history plays a major role in your credit score. Missing even one EMI:

- Sends a negative signal to credit bureaus

- Lowers your score

If you already have a low CIBIL score, this can make things worse and limit your financial options.

4. Future Loan Approvals Become Difficult

Lenders look at your past behaviour before approving new loans.

A missed EMI can:

- Reduce your chances of getting approved

- Affect your loan eligibility criteria

- Lead to higher interest rates

Even if you were eligible for a pre-approved loan, that offer might disappear after a missed payment.

5. Increased Financial Burden

Here’s something many borrowers don’t realise:

Missing an EMI doesn’t pause your loan; it makes it more expensive.

- Interest keeps adding up

- Penalties increase your total cost

- Your repayment period may feel heavier

Over time, this affects your ability to manage other financial goals like savings or tax savings planning.

6. Constant Follow-Ups from Lenders

If the payment is not cleared quickly:

- You’ll start receiving reminder calls, SMS, and emails

- Lenders may follow up regularly

While this is standard procedure, it can become stressful if delays continue.

7. Serious Consequences After 90 Days

If you miss EMIs for a longer period (usually 90 days):

- Your loan may be categorised as a default

- Your credit profile is severely impacted

At this stage, rebuilding your financial reputation becomes much harder.

Related blog: Pay Off Your Personal Loan Early Foreclosure Charges, Steps & Benefits

How to Avoid Missing Your EMI?

Missing an EMI usually doesn’t happen intentionally; it’s often the result of poor planning or timing issues. The good news is that with a few smart habits, you can easily avoid it.

Start by using a personal loan calculator before taking a loan. This allows you to choose an EMI amount that aligns with your income and expenses. Avoid the temptation to borrow the maximum amount you’re eligible for; just because you qualify doesn’t mean you should take it. Maintaining a buffer in your bank account is another simple but powerful strategy. Always keep enough balance to cover at least one EMI, especially if you rely on auto-debit. This is crucial for salaried employees, where timing mismatches between salary credits and EMI dates are common.

Automation also helps. Set up auto-debit instructions and add calendar reminders as a backup. Even though payments are automatic, reminders ensure you’re always aware of upcoming deductions. Choosing the right tenure plays a big role, too. A longer tenure reduces your EMI burden but increases overall interest, while a shorter tenure does the opposite. Finding the right balance is key to avoiding repayment pressure.

You should also understand the terms of your loan, especially if you’re using options like a pre-approved loan or a flexi personal loan. These may offer convenience and flexibility, but they still require disciplined repayment.

Finally, always keep track of your financial health. If you already have a low CIBIL score, missing EMIs will worsen your situation and reduce future borrowing opportunities.

Recent blog: How to Decide the Best Tenure for Your Instant Personal Loan

What Should You Do If You Have Already Missed an EMI?

If you’ve missed an EMI, the worst thing you can do is ignore it. But the good news is, if you act quickly, you can limit the damage and regain control of your finances. The first step is to pay the missed personal loan EMI as soon as possible. The longer you delay, the more penalties and interest will accumulate. Even a short delay can increase your total repayment cost and put unnecessary pressure on your finances.

Next, inform your lender. Many borrowers hesitate to do this, but early communication can actually work in your favour. Lenders may offer temporary solutions like adjusting your EMI date or giving short-term relief, especially if you have a good repayment history. You should also review your finances immediately. Try to understand why the EMI was missed. Was it due to poor planning, unexpected expenses, or insufficient funds? Once you identify the cause, you can take corrective steps to avoid repeating the mistake.

This is also a good time to do a quick loan comparison. Evaluate whether your current loan terms, interest rate, tenure, or EMI amount are still suitable for your financial situation. Sometimes, switching to better terms or refinancing can ease your repayment burden.

If you’re facing genuine financial stress, speak to your lender about restructuring options. This could include extending your tenure or reducing your EMI amount to make repayment more manageable. Some borrowers consider short-term solutions like payday loans to cover missed EMIs. While these may offer quick cash, they often come with very high interest rates and should be used cautiously. Relying on such options repeatedly can worsen your financial situation instead of solving it.

It’s also important to check your credit report after a missed EMI. This helps you understand how much your score has been impacted, especially if you already have a low CIBIL score or are planning to apply for loans in the future.

Most importantly, avoid repeating the mistake. One missed EMI can be managed, but repeated delays can seriously affect your loan eligibility criteria, reduce your chances of getting a pre-approved loan, and limit access to better loan types.

Might you have missed: NBFC vs Bank Personal Loan: Which Is Better for Quick Approval?

Conclusion

Missing a personal loan EMI may seem like a small mistake at first, but it can quickly turn into a bigger financial issue if not handled properly. From penalty charges and credit score impact to reduced loan eligibility and higher borrowing costs, the consequences can affect your overall financial stability.

The key is to stay proactive. With the help of a personal loan calculator, proper planning, and disciplined repayment, you can avoid most EMI-related issues. And even if you do miss a payment, acting quickly by paying dues, communicating with your lender, and reviewing your finances can significantly reduce the damage.

Whether you’re a salaried employee, a first-time borrower, or exploring different loan options like pre-approved loans, responsible repayment should always be your priority. Smart borrowing today ensures better financial opportunities tomorrow.

Don’t let EMIs surprise you. Calculate, compare, and choose the best loan with Loan Quantum.

Frequently Asked Questions

Most lenders charge penalties immediately after the due date is missed. There is usually no grace period, so it’s best to pay as soon as possible.

Pay the overdue amount as soon as possible, inform your lender, and ensure you don’t miss the next payment to avoid further penalties.

Payday loans provide quick cash but come with very high interest rates. They should only be used as a last resort, as they can increase your financial burden.

Yes, due to penalties and additional interest, your overall repayment amount increases if you miss EMIs.

An EMI delay is when you miss a payment but clear it within a short time. A default happens when EMIs remain unpaid for a longer period (usually 90 days), severely impacting your credit profile.